Picture this—a slow morning with a sip of tea, enjoying time with loved ones without worrying about financial condition—that’s all our senior citizens crave. After all, what else do they want to make their life memorable in this phase except a comfortable living with their loved ones?

SBI (State Bank of India) Home loans for senior citizens emerge as one of the most efficient financial assistance options for them to live comfortably for the rest of their lives. As a dedicated scheme for senior citizens, the SBI Reverse Mortgage Loan (the latest SBI Home Loans scheme for senior citizens) emerges as an additional income source provider for senior citizens in India, by using one of their productive assets, the home.

This post is dedicated to describing the SBI Reverse Mortgage Loan, covering interest rates, the application process, and important tips to remember while availing of this loan.

Highlights for SBI Reverse Mortgage Loan

| Loan Type | Reverse Mortgage Loan for Senior Citizens |

| Loan Tenure | 10 – 15 years |

| Loan Amount | Up to Rs 2 crore for metro cities Up to Rs 1.5 crore for other cities |

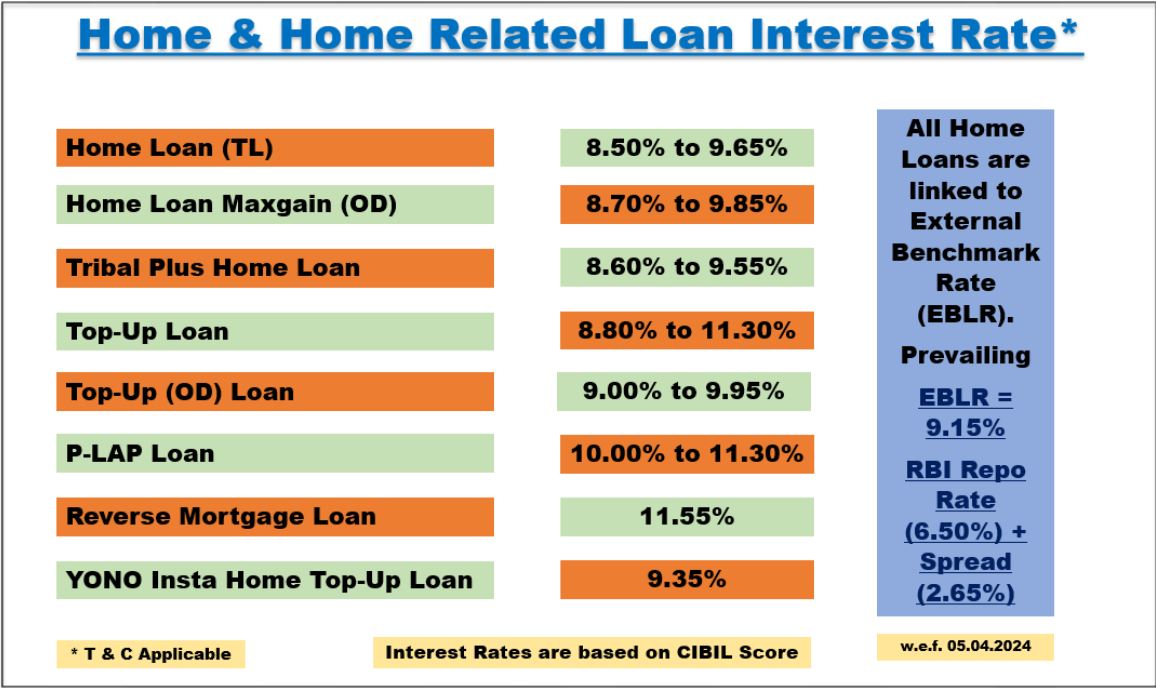

| Interest Rates | 11.05% p.a. (linked to external benchmark rate) |

| Processing Fee | 0.50% of the loan amount Minimum: Rs 2,000 Maximum: Rs 20,000 Including applicable taxes |

| Ownership Status | The property must be named after the borrower |

Introducing the Reverse Mortgage Loan

The Reverse Mortgage Loan is a unique service offered to Indian senior citizens. In this scheme, they receive a fixed periodic income on a monthly, quarterly, or lump sum basis in exchange for mortgaging their residential property.

To clarify, this mortgaged property will still be available for them to live in for the rest of their life, and also, this transaction doesn’t feature any loan repayment obligations during their lifetime. In case of the borrower’s demise, SBI can sell the property for dues recovery, or heirs can repay the loan for property retention.

Features and Benefits of SBI Reverse Mortgage Loan

The following are some notable features and benefits offered by the SBI Reverse Mortgage Loan:

- No Repayment Required in Lifetime Duration: This is one of the soothing features for borrowers as they don’t need to repay the loan in their lifetime duration.

- Home Stay in the Mortgaged Property: Senior citizens can continue to stay in their mortgaged property without worrying about the bank’s interventions.

- Fixed Income Stream: Reverse Mortgage Loan provides senior people with a fixed income stream (monthly/quarterly payments) to fulfill their personal needs on their own.

- Low Interest Rates: Due to the SBI’s competitive interest rates, it becomes possible for senior people to preserve their property’s value for a longer duration and ensure better returns from the loans.

- Low Processing Fee: SBI Reverse Mortgage Loan features a minimal processing fee without any hidden charges and prepayment penalty.

Interest Rates and Processing Fees

This SBI Home Loan scheme for senior citizens features interest rates of 11.05% based on CIBIL score. It is linked to the external benchmark rate (EBLR), which is (as of writing) 8.65%.

For this scheme, SBI charges a processing fee of 0.50% of the loan amount. The minimum and maximum charges are Rs 2,000 and Rs 20,000, respectively, plus applicable taxes.

Moreover, there are post-sanction charges associated with the SBI Reverse Mortgage Loan, which are mentioned below:

- Stamp Duty: Varies state-by-state for the loan agreement.

- Property Insurance Premium: For property safety purposes.

- CERSAI Registration Fee: 1) For loans up to Rs 5 lakh – Rs 50 + GST; 2) For loans above Rs 5 lakh – Rs 100 + GST

Eligibility Criteria

- The borrower must be an Indian resident.

- The minimum age is 60 for a single borrower and 58 for a spouse in a joint borrower’s application.

- The residential property that will be mortgaged should be named after the borrower.

- Properties located nationwide are available for mortgage to SBI, offering higher funds for metro cities.

- Properties that are in litigation or have been inherited but are not properly registered in the applicant’s name are ineligible.

Documents Required

| Basic Documents | Property Documents |

| Duly filled loan application form with 3 passport-size photographs attached For Identity Proof, any one of the following: PassportVoter ID CardPANDriving License For Address Proof, any one of the following: Water BillElectricity BillTelephonic Bill’s recent copyPiped Gas BillPassport or Driving License (in case they are not used as ID proof) | Registered Sale Deed and Link Documents for Title Tracing Certificate of Occupancy (preferred but optional) Property Tax Receipt, Maintenance Bill, Electricity Bill, and Share Certificate (exclusive to Maharashtra) Conveyance Deed, the builder’s Registered Development Agreement, and an approved copy of the plan (Xerox blueprint) |

Application Process for SBI Reverse Mortgage Loan

To apply for the SBI Reverse Mortgage Loan, interested applicants have both offline and online options to choose from. Let’s get a quick snapshot of both options, one by one:

Via Offline Mode

- Interested applicants need to visit their nearest SBI branch.

- Collect all the required documents.

- Get in contact with the branch’s manager or officer.

- Start the application process with the help of banking professionals.

Via Online Mode

Here’s how you can apply for the SBI Reverse Mortgage Loan online mode for your senior citizens:

- Step 1: Go to the official page of the SBI Home Loan Application form.

- Step 2: Here, you must go through different forms and fill out the required information. The following points refer to those forms and what needs to be filled out there:

- FORM – A: Fill in your senior citizens’ personal details, including name, PAN, KYC, Date of Birth, Contact Information, and marital status.

- FORM – B: This section requires their employment status and income details to assess their loan repayment capacity.

- FORM – C: Details like property specifications, loan tenure, amount, etc, should be filled in this section.

- FORM – D: This is a declaration to confirm the agreement after reading and signing it (declaration).

- Step 3: Collect all the required documents and submit them after completing the application.

- Step 4: As the submission of all the required documents takes place, SBI starts application processing. A loan sanction letter will be sent to you on successful application approval.

Difference Between SBI Reverse Mortgage Loan and Regular Home Loan

The following table clarifies the uniqueness of the SBI Reverse Mortgage Loan in comparison to regular home loans:

| Differentiative Factors | SBI Reverse Mortgage Loan | Regular Home Loans |

| Purpose | Specifically designed for senior citizens who are the owners of a residential property and need financial support without selling it. | Provides for multiple purposes, such as buying a home, constructing a home, etc. |

| Repayment | Repayment doesn’t take place until the borrower’s demise or their heirs prefer to settle the loan. | A consistent repayment continues throughout the loan tenure through EMIs. |

| Eligibility | Only senior citizens are eligible, with a minimum age of 60 years for single applicants and 58 years for spouses in joint applications. | Available for salaried and self-employed individuals (typically prefer young professionals) with stable income and a satisfactory credit history. |

| Loan Tenure & Amount | Features loan tenure of up to 10 – 15 years and maximum loan amount of up to Rs 2 crore for metro cities and Rs 1.5 crore for other cities. | It features comparatively longer loan tenures and higher loan amounts, as per the borrower’s eligibility and the credit policy of the lender. |

| Property Ownership | Senior citizens retain ownership of their mortgaged property and continue to stay there for their lifetime. | Ownership of a new property with regular home loans often comes with consistent payment of allotted EMIs by the lender throughout the tenure. |

| Amount Disbursement | The amount disbursement takes place in this scheme on a monthly, quarterly, or lump sum basis in exchange for mortgaging your residential property to the SBI. | In regular home loans, the sanctioned loan amount is disbursed as per the lender’s credit policy and purchase agreement or construction status to buy, construct a house, etc. |

Important Tips to Remember

To really enjoy the perks of the SBI Reverse Mortgage Loan, senior citizens must know some important facts about this scheme:

- Repayment for this scheme is only required when you pass away, sell the property, or move out permanently.

- SBI doesn’t provide full property value as a loan. It provides approximately 55-60% of the property’s market value.

- Any other loan can’t be taken on this mortgaged property due to the fixed tenure.

- The heirs receive the surplus if the property sells for more than the debt.

- The income you receive through this scheme is not subject to tax consideration under Section 10(43) of the Income Tax Act, 1961.

- SBI’s appointed valuer will value your property.

- Your heirs can inherit the property. However, they must repay the loan, which can be accomplished by selling the property or other means.

- Interest accumulation is also something you must consider throughout the loan tenure, as it can increase the total loan amount and reduce the equity you hold in your property.

References:

SBI Reverse Mortgage Loan – Income for Seniors [2025]

SBI Reverse Mortgage Loan: Income After Retirement in India

{kind=link}